Three in five (60%) small businesses with longer payment terms face cash flow problems. In contrast, businesses offering immediate payment terms report a much lower rate of just 40%. This difference highlights a critical challenge: accurately recording cash received on account is vital for businesses managing credit-based sales.

Properly tracking cash receipts not only strengthens cash flow but also ensures accurate financial reporting. Businesses can improve internal controls, maintain compliance, and make data-driven choices that increase growth by accurately recording cash received on account.

In this article, we’ll explore how to effectively manage and record these transactions for better financial management.

Accurately recording cash received on account is essential for maintaining healthy cash flow and financial integrity. To make sure your records are correct, use double-entry accounting, clear narrations, and regular reconciliations. SECS Inc. provides solutions that ensure adherence to industry standards, minimize past-due accounts, and streamline receivables management.

Cash received on account is a payment made towards a customer’s outstanding balance, reducing the accounts receivable. This transaction is tied to previous credit sales, where payment is made after the sale, not at the point of purchase. It's crucial for precisely tracking financial transactions and monitoring customer payments.

Unlike cash sales, where payment is made immediately, cash received on account happens after a credit transaction. While cash received on account lowers the amount owed from previous transactions, cash sales result in an instant payment with no outstanding balance.

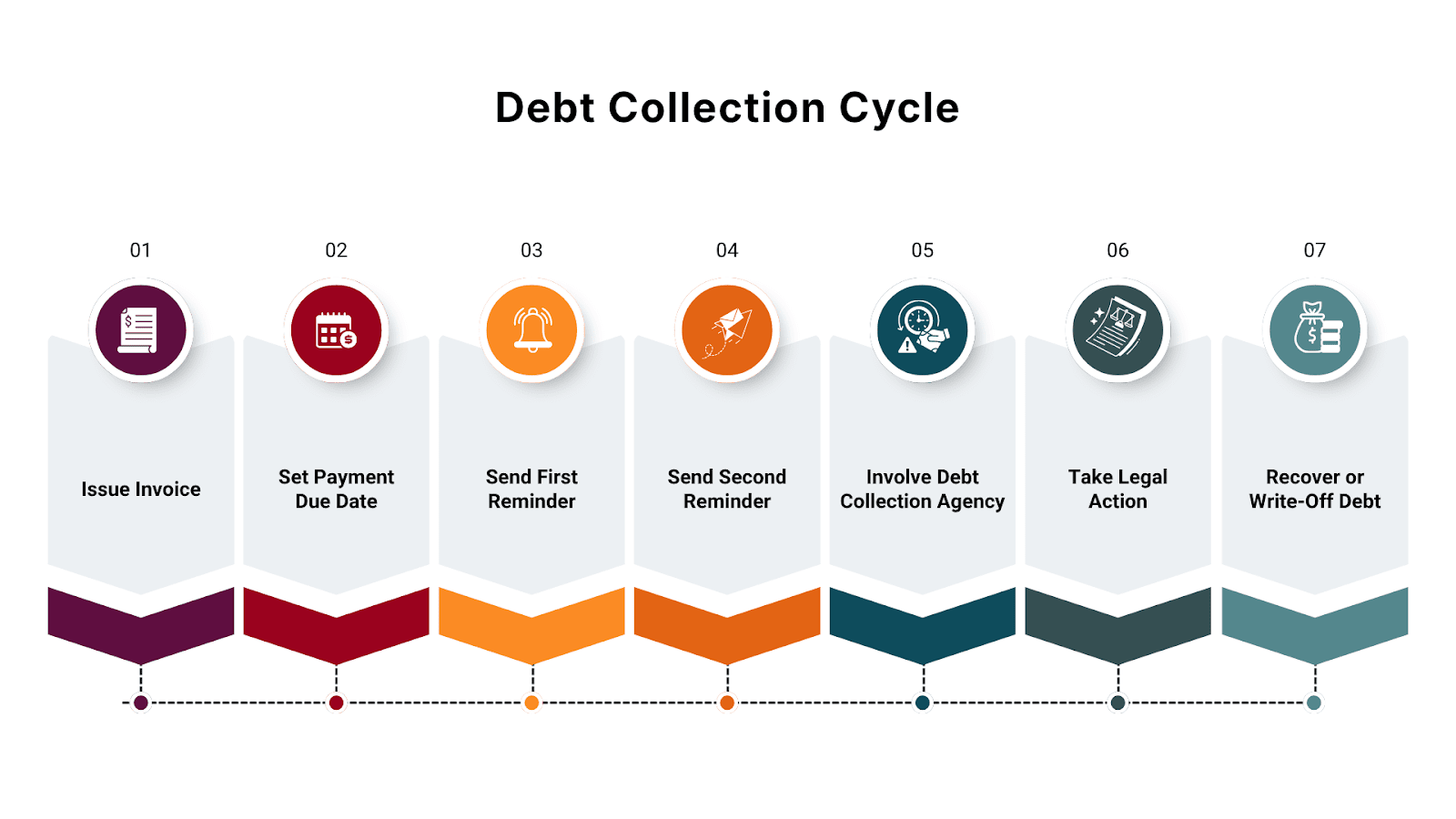

The above image illustrates the Debt Collection Cycle, outlining each step from invoice issuance to debt recovery or write-off, helping businesses manage overdue accounts effectively.

Example:

You sold products worth $10,000 to a customer on credit. When the customer pays $5,000, that payment is called cash received on account, because it partially settles the credit. The remaining $5,000 is still recorded as accounts receivable until fully paid. This distinction helps track what has been received versus what is still owed.

As we move forward, understanding how these transactions affect your accounts is crucial for accurate journal entries and maintaining organized financial records.

To record cash received on account accurately, you must identify the key accounts impacted by the transaction. The two primary accounts that will be impacted by this transaction are cash and accounts receivable.

Example Journal Entry:

Also read: Understanding the process of receiving cash from an account receivable

Once you have a clear understanding of the affected accounts, the next step is applying the double-entry accounting system to ensure the transaction balances correctly.

Late payments significantly impact small businesses, with 50% of companies facing cash flow problems and those with more past-due bills being 1.4 times more likely to experience these issues. Ensuring accurate accounting is essential to avoid these disruptions.

To keep accurate financial records, the double-entry accounting system is essential. When cash is received on account, crediting the accounts receivable lowers the amount your customer owes, while debiting the cash account increases the cash balance. This ensures that your accounts remain transparent and balanced.

Double-Entry Breakdown:

With the double-entry system in place, the next step is understanding how to properly document your entries with clear narrations for better tracking and clarity.

After recording your cash received on account entry, make sure to add an effective narration for clarity. Include details such as the payer, date, and purpose of the transaction. Clear narrations make future reviews or audits easier to follow and provide context for each transaction. This helps distinguish between transactions and improves transparency.

Example of Effective Narration:

Also read: How an Increase in Accounts Receivable Affects Cash Flow

After creating clear narrations, ensure you enter your transaction in the correct journal and then post it to the appropriate ledger for accurate record-keeping and audit efficiency.

Small businesses affected by late payments are 1.4 times more likely to have raised prices recently (30% vs. 21%). Their average price increase is 16%. Recording funds received on account accurately is important. This process helps ensure cash flow and corporate stability and prevents financial strain.

It is important to enter cash received on account into the right journal. Most of these transactions go into the Cash Receipts Journal. Smaller businesses may use the General Journal, especially if transactions combine sales or deposits.

Example:

If a customer pays $5,000 towards their outstanding balance, the journal entry will look something like this in the Cash Receipts Journal:

After journalizing, the next step is posting the transaction to the General Ledger and the Subsidiary Ledger. This ensures that the accounts are current and that the financial status of your company is accurately reflected in your records.

Example:

Maintaining accurate ledgers is key to keeping your records correct. After posting the entries, it's important to reconcile your records to ensure they match external statements and uncover any discrepancies. This step highlights the importance of regular reconciliation.

Reconciliation is crucial for maintaining the integrity of your financial records. You can quickly identify and correct inconsistencies before they become serious problems by routinely comparing your cash receipts on account with your cash sheets and bank deposits.

It's similarly critical to keep an eye on accounts receivable aging data. These reports enable you to monitor past-due payments and take prompt action. The longer an account remains unpaid, the harder it becomes to recover, potentially impacting your cash flow.

Pro Tip: Set up daily reconciliation routines to prevent errors from piling up. Discrepancies are easier to resolve the earlier they are discovered. By being proactive, you can avoid more serious issues later on and save time.

Also read: Managing Delinquent Account Receivables Effectively

You can ensure the accuracy of your financial records and the effectiveness of your collections operation by regularly monitoring your receivables. This is where SECS Inc. can assist, providing automated solutions to help streamline and manage your receivables more effectively.

South East Client Services Inc. (SECS Inc.) helps businesses effectively manage their receivables through a range of personalized services designed to streamline the process and ensure accurate financial records.

Here is how SECS Inc. can help:

These services provide businesses with a more efficient, accurate, and compliant approach to managing receivables.

Accurately recording cash received on account is vital for maintaining proper financial records and ensuring healthy cash flow. Businesses should stay on top of their receivables and prevent inconsistencies that could impact their operations by adhering to procedures, including double-entry accounting, transparent narrations, and prompt reconciliations.

SECS Inc. provides businesses with streamlined solutions to manage their receivables more efficiently. SECS ensures that your collections process operates efficiently, lowering past-due accounts and guaranteeing accurate financial reporting with their advanced technology and compliance-focused services.

Ready to improve your receivables management? Contact SECS today and take control of your cash flow with a solution personalized to your business needs.

A. To properly track cash received on account, ensure that you're recording the payment against the correct customer's outstanding balance. Debit your cash account and credit accounts receivable using double-entry accounting. For accuracy, reconcile these records on a regular basis with bank statements and cash sheets.

A. To identify inconsistencies early, it is advised to reconcile funds received on account every day. By ensuring that your cash receipts match your cash sheets and bank deposits, daily reconciliation helps to improve overall financial accuracy by preventing errors from building up.

A. Clear narrations provide context for each transaction, helping maintain transparency and ensuring that audits or future reviews are straightforward. This method helps to differentiate between different transactions over time and makes it simple to follow the purpose of each entry.

A. Regularly monitor accounts receivable aging reports to identify overdue payments. Prioritize collections by focusing on older accounts first. To increase cash flow and streamline the collection process, consider implementing automated reminders and follow-ups.

A. Laws such as the Telephone Consumer Protection Act (TCPA) and the Fair Debt Collection Practices Act (FDCPA) must be followed when collecting debt. These rules ensure that companies collect debts fairly and lawfully while protecting customers from unfair practices.

This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose.

.jpg)