Have you ever received a debt collection notice and wondered if it was even yours? This simple letter could be your first line of defense. A debt validation letter is a written request asking a debt collector to verify that the debt they are attempting to collect is legitimate.

Without this tool, you run the risk of paying for something you don't owe or providing false information that could lower your credit score.

In 2024, the CFPB received over 102,000 complaints related to debt collection, many of which involved disputes over the validity of debts. This highlights how common and important debt validation can be.

In this article, we'll guide you through how to draft a debt validation letter and why it's crucial for your financial stability.

TL;DR

You have 30 days from the date of the debt collector's initial contact to obtain this validation under the Fair Debt Collection Practices Act (FDCPA).

When you receive an unexpected or unclear debt notice, it's crucial to send this letter. In addition to preventing additional collection efforts, sending it within 30 days of the initial contact allows you to have time to determine whether the debt is legitimate or if an error occurred.

By asking for validation, you can ensure the debt collector has the proper paperwork to support their claim.

Now that you understand when to send a debt validation letter, let's look at how to write one effectively.

Once you know what to include, writing a debt validation letter is simple. Here's a quick guide to make sure you include all the important details:

Gather any relevant data regarding the debt, such as the account number, the amount owing, and the contact details of the debt collector, before you start writing your letter. This guarantees that you mention specific details in your letter.

A clear request for debt validation should be made at the start of your letter. Request specific documents, including the original signed contract, the amount owing, and evidence of the debt collector's authority to collect the debt.

Avoid emotional language or confrontational tones in your letter. Keeping the tone professional will help you maintain control of the situation and prevent escalating the matter.

Request details about the debt, including the original creditor, a breakdown, and evidence of the collector's legal authority to pursue the debt. This ensures that you have all the data you need to assess the legitimacy of the debt.

Pro Tip: To ensure proof of delivery, send your debt validation letter by certified mail at all times. This way, you can defend yourself and have evidence that the debt collector received your request.

Also read: Understanding the Pay for Delete Method in Debt Collections

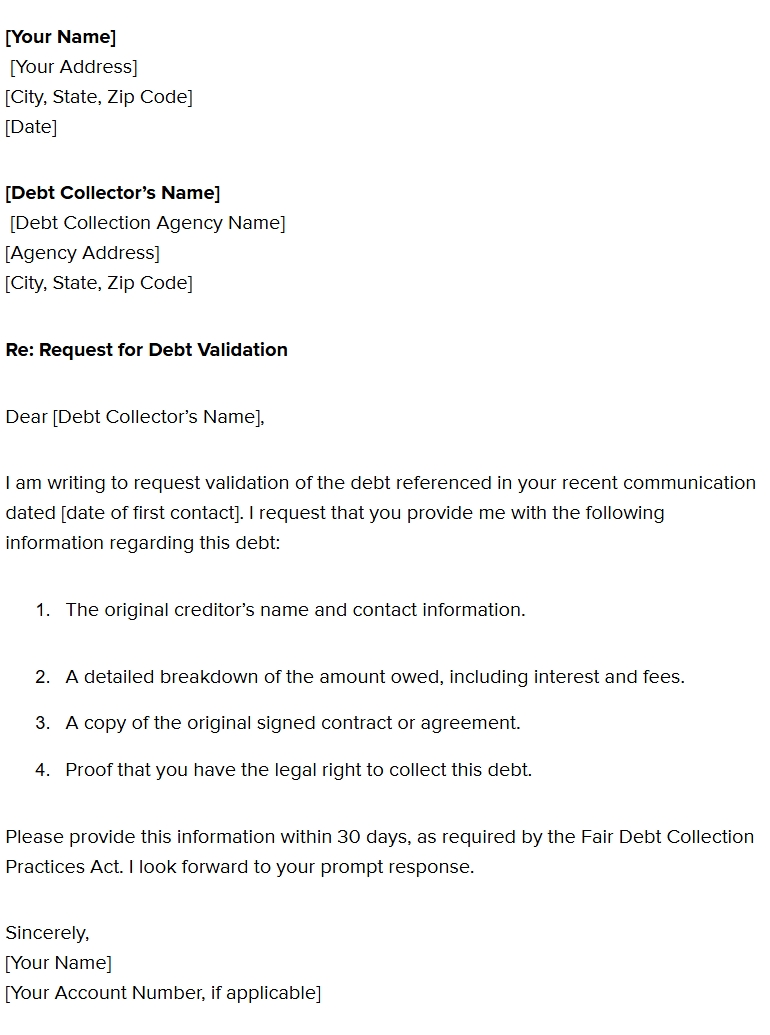

Now that you know how to write the letter, let's look at a sample you can use as a template.

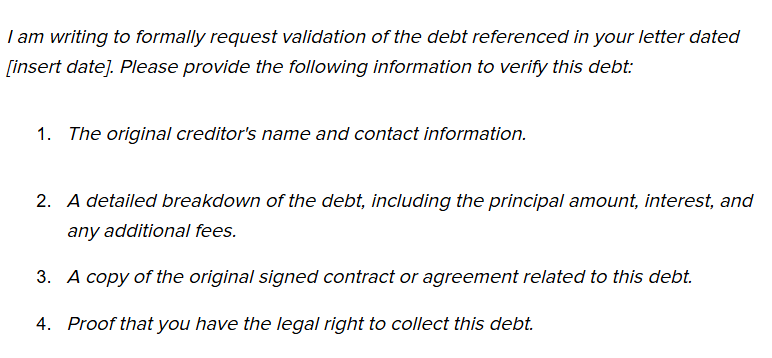

Here’s a sample Debt Validation Letter that you can customize to fit your situation:

This sample letter covers the key elements of a debt validation request. By following this template, you ensure that your letter is clear and direct, increasing your chances of receiving the necessary documentation. Let's discuss what to include in your letter to ensure you've covered all the bases.

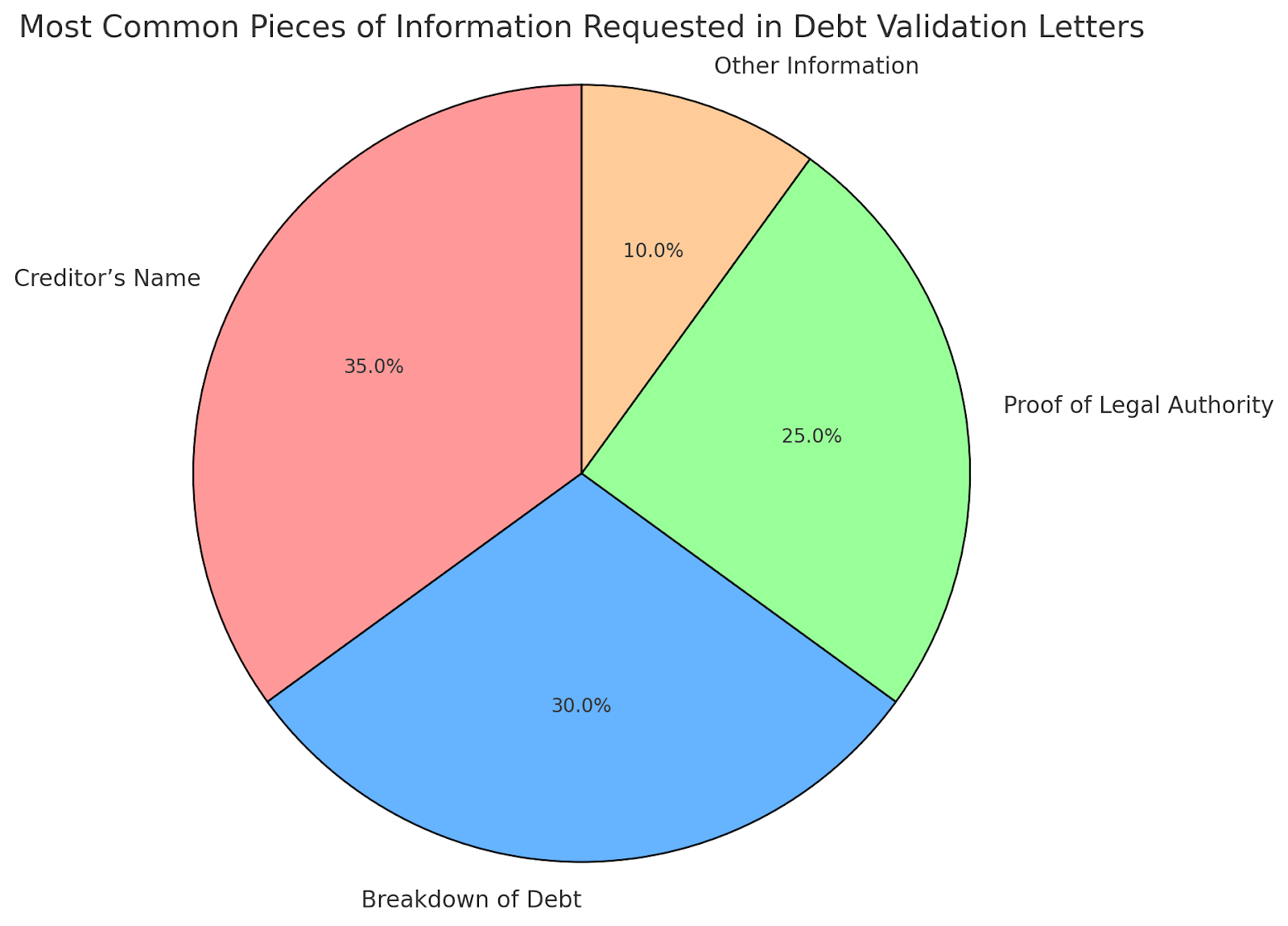

Make sure your debt validation letter contains the following key components to avoid confusion and ensure the debt collector understands your request:

The above chart shows the most common pieces of information requested in debt validation letters.

Make it clear that you are requesting validation of the debt. Use direct language such as, “I request that you validate this debt by providing the following…”

Request a detailed explanation of the debt, including the initial principal, interest, and additional fees. This will ensure that the reported quantity is accurate and assist you in understanding the validity of the whole amount.

Get information about the original creditor, such as their name, address, and phone number. You can use this information to confirm if the debt is real and linked to a respectable creditor.

Pro Tip: The debt collector is legally prohibited from pursuing the debt if they do not deliver the necessary details within 30 days. This allows you to cease all additional collection efforts until the required paperwork is submitted.

Understanding the next steps after sending the debt validation letter is critical. Let's discuss potential responses and what to do once the letter has been sent.

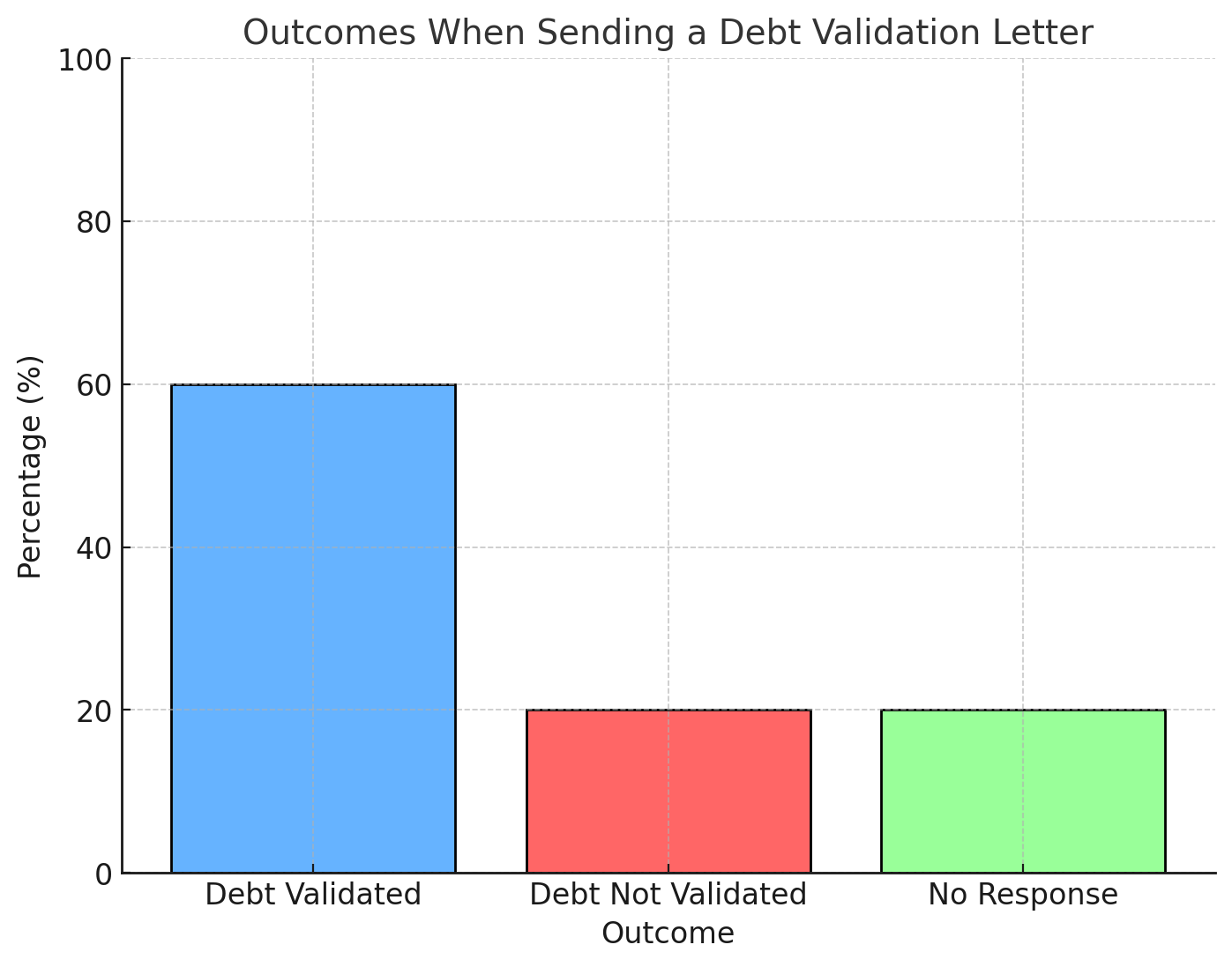

The debt collector must reply within 30 days of receiving the debt validation letter. There are two possible outcomes you might encounter:

The above graph compares the outcomes when sending a debt validation letter. The data shows that in the majority of cases, debt collectors either validate the debt or cease collection efforts after receiving the debt validation letter within 30 days, as per the Federal Trade Commission.

The debt will be verified if the collector submits the required paperwork. You can proceed with debt resolution in this situation. This could entail settling the debt for a reduced sum, negotiating a payment schedule, or setting up other terms that work for your budget.

The debt collector has to cease collection attempts if they cannot produce sufficient documents within 30 days. You are under no obligation to pay at this time, and the collector cannot pursue the claim further without the necessary proof. You might be able to file a lawsuit if they continue without proper documents.

Pro Tip: Don't be afraid to negotiate if the debt has been verified and you cannot make the entire amount. Many collectors are willing to accept a payment plan or settle the debt for less. It's always worth asking for more manageable terms.

Also read: Understanding Your Rights Against Debt Collector Harassment

Now that you know the potential outcomes, knowing when to get legal help is critical, particularly if your rights are violated. Let's look at scenarios where legal assistance may be necessary.

It could be time to consult a lawyer if the debt collector acts aggressively or refuses to produce the required paperwork. In the following circumstances, you should consider getting legal assistance:

Are you unsure of your rights or need assistance handling a debt dispute?

With more than 30 years of experience in receivables management, South East Client Services Inc (SECS Inc) provides companies with transparent and compliant solutions. They specialize in offering expert guidance and help navigate complex debt problems, ensuring that your financial interests are protected at every stage.

Now that you understand the process and know when to seek help, let's conclude with a last summary of the significance of employing a Debt Validation Letter.

A Debt Validation Letter is vital to ensure that any debt collection efforts are legitimate. By requesting proper paperwork, you keep control of your finances and protect against paying incorrect or fraudulent debts. You can protect your credit and prevent expensive errors by being aware of your rights and promptly acting.

South East Client Services Inc (SECS Inc) provides all-inclusive receivables management and debt recovery solutions for businesses. SECS specializes in portfolio management, portfolio acquisitions, and compliance-driven debt recovery.

Their services are designed to assist companies in managing past-due accounts, enhancing cash flow, and reducing risk while adhering to industry standards.

If you're dealing with a debt collection issue or need assistance navigating your rights, contact SECS Inc right now to take charge of your financial future.

Q. How can I ensure my Debt Validation Letter is received by the debt collector?

A. To ensure your Debt Validation Letter is received, send it via certified mail with a return receipt request. In order to resolve a dispute if necessary, this serves as proof of delivery, attesting that the debt collector received your letter.

Q. What should I do if the debt collector doesn't respond within 30 days?

A. The debt collector must stop all collection efforts if they don't reply within 30 days. You can stop payments until they provide the required validation. If they persist without proof, file a complaint with the CFPB or consult a lawyer.

Q. Can I dispute the debt after receiving the validation?

A. Yes, even after receiving confirmation, you have the right to contest the debt if you think it is inaccurate or fraudulent. In order to protect your rights and resolve inconsistencies, ask for additional documents if necessary or consider getting legal counsel.

Q. What if the debt collector sends me incomplete or insufficient documentation?

A. If the documentation is incomplete, the debt collector must cease collection efforts. Request additional information or clarification. If they continue without proper validation, you may need to file a complaint or seek legal advice.

Q. Can I use a Debt Validation Letter to stop a debt collector from calling me?

A. Yes, sending a Debt Validation Letter can stop calls if they fail to validate the debt within 30 days. You can also send a "cease and desist" letter, which legally requires the collector to stop contacting you, to fully discontinue communication.

This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose.

.jpg)